It’s that time of year when the whole “new year, new you” PR machine kicks into high gear. And while the idea of trying to embrace a slew of resolutions at once feels overwhelming, introducing a couple of new healthy habits can do you good. They don’t have to be food- or exercise-related if that isn’t what you’re into. Instead, consider your financial health. What are your financial goals in 2024? If you don’t have any yet, we’re here to help. Consider it your “Krazy Era.”

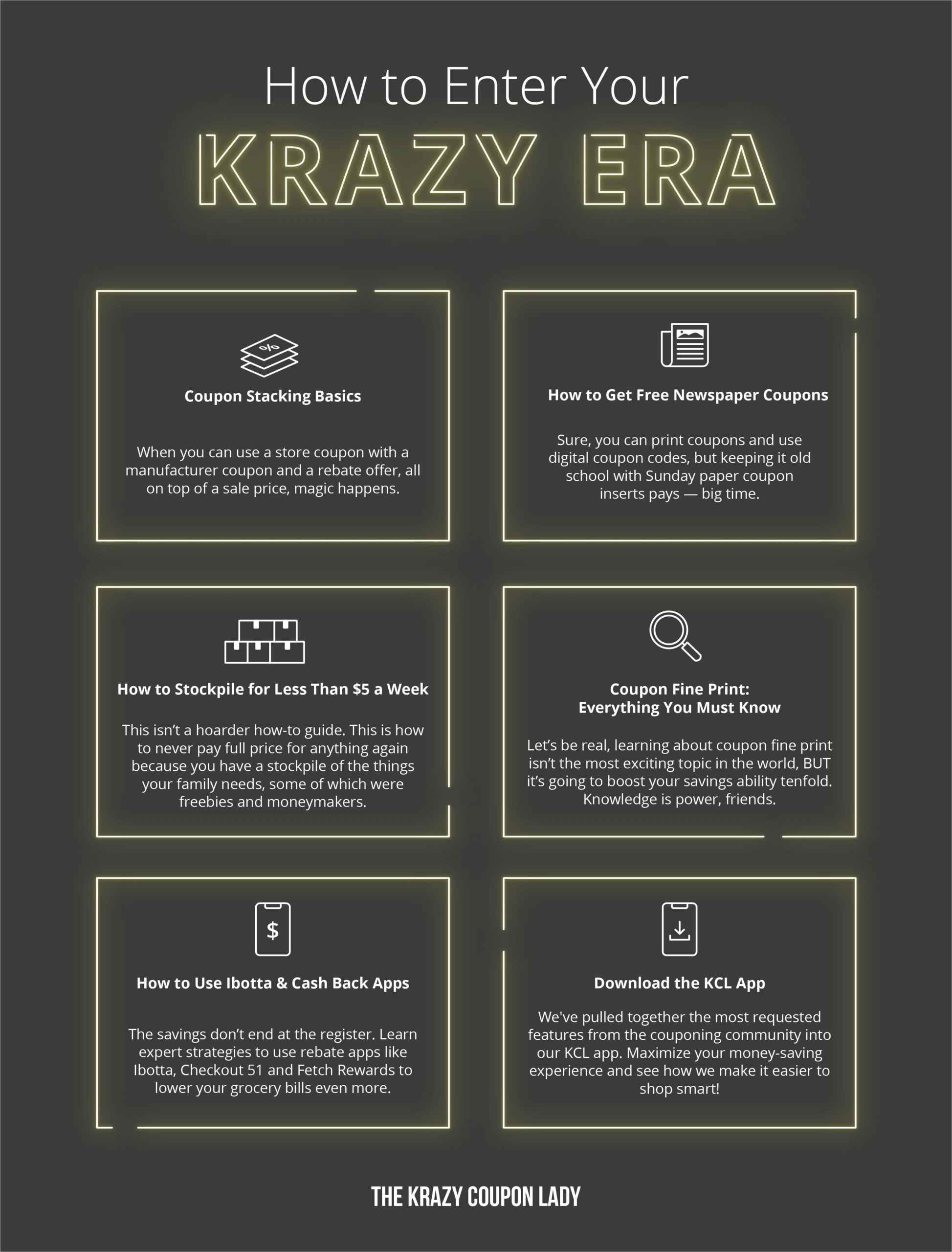

What the heck is the Krazy Era? It’s saving whenever, wherever you can. If you don’t already know how to stack coupons, that’s one lesson. Using Ibotta and other cash-saving apps is another. Basically, this is your time to learn all about keeping as much money in your wallet as possible without sacrificing the things you enjoy.

We asked two experts to weigh in on setting financial goals this year, and she came back with some fantastic advice. Keep reading to find out where to start, and make sure you download The Krazy Coupon Lady app to get money-saving hacks sent to your phone.

Yes, you can reach financial goals in 2024.

Rome wasn’t built in a day, and the same goes for a robust personal finance situation. If your savings account feels low (or nonexistent), there’s never been a better time to get started.

1. Create a strategy.

Without a map (or GPS), you can’t reach a new destination, right? Well, the same can be said for your financial goals. If there isn’t a plan in place, it’s nearly impossible to set and meet a goal.

“The only and first place to start is to create a budget and stick to it,” says Pattie Ehsaei, who teaches financial literacy on her TikTok channel Duchess of Decorum, in an interview with The Krazy Coupon Lady. “Utilize online budgeting tools that allow you to customize your budget based on your income, spending needs, and financial goals.”

Some of our favorite free budget apps include Mint, Personal Capital, and Digit, but the one that’s best for you really depends on your individual needs.

Related: Healthy Deals for 2024

2. Abide by the 50/30/10/10 rule.

Cool apps aside, when it comes to creating a budget, Ehsaei encourages using the 50/30/10/10 rule. The concept breaks down like this:

50% of your income should go toward your needs (rent, utiltities, things you need to survice)

30% to your wants (play money)

10% to your savings

10% to your emergency fund.

“When you have 3 – 6 months of living expenses in your emergency fund, that 10% should go into your savings,” Ehsaei says.

3. Contribute to your 401k as early as possible.

One of the best pieces of financial advice Ehsaei personally received involves building a 401k — the sooner, the better.

“Most don’t understand how 401ks work and think they can’t afford to contribute,” she says. “Nothing is further from the truth. First, the money contributed to your 401k is pre-tax money. That means, since you’re not paying tax on those dollars, the impact on your take home pay is minimal.”

Moreover, employers will usually match a certain percentage of your own 401k contribution. This means free money,

“That’s money you’re leaving on the table if you do not participate in your 401k plan,” Ehsaei says.

4. Choose your financial goals.

You’re in the driver’s seat here. Decide ultimately what your financial goals are for this year. In the short-term, these can include starting an emergency fund, reducing your debt, and even simply setting a budget and actually sticking to it. Look to the 50/30/10/10 if you don’t know where to begin with a budget.

Related: 35 Free Date Ideas

5. Get a little aspirational.

“When it comes to making financial goals, make them sticky,” Tori Dunlap, author of Financial Feminist, tells The Krazy Coupon Lady.”What I mean by that is they should feel just lofty enough that you’re a little worried you won’t be able to reach them, but not so low that you have absolutely zero doubts.”

Do you want to stick to a budget? Are you trying to max out your Roth IRA? Dunlap suggests creating a tangible plan that you can hold yourself to from month to month.

Related: Free Budget Printables

6. Check in with the status of your finances regularly.

Don’t just create some goals for the sake of it and then hope the universe wills it to happen. This might not be the sexiest sounding date, but Dunlap thinks you should schedule regular times to go over your financial goals.

“Create regular ‘money dates’ with yourself to check in and track your progress,” she says.

7. Get a little invested.

When Dunlap was getting her finances in order, a wise person suggested she start investing as soon as possible.

“The best way to build wealth is to invest in the stock market, which is why I encourage people to join my investing app, Treasury,” she says. “It takes the intimidation out of investing and makes it easy to learn how to begin investing.”

Ultimately, Dunlap says investing is important because you gain compound interest.

“The average rate of return in the stock market is about 7-10 percent. You’ll likely make that interest and then make interest on that interest and so on and so forth,” she says. “It’s the best way to set yourself up for retirement and it was an essential part of how I was able to save my first $100K.”

8. Learn how to reduce debt effectively.

When you’re looking at a pile of bills, some overdue, the stress feels overwhelming. If there’s any wiggle room to negotiate existing bills but you’re not exactly a negotiator, try using a service like BillCutterz. The name says it all; they will actually do the negotiating for you. Of course, they aren’t doing this out of the goodness of their hearts. However, if they manage to reduce one of your bills to a lower price, you split the savings with them for one year. After that, the savings is yours and yours alone.

However, to reduce debt on your own, pay more than the minimum required whenever possible, or pay more than once a month.

9. Get chummy with cash back apps.

Not to sound like a broken record, but rebate apps like Ibotta can really put a healthy amount of money back in your wallet. We have a whole article about how Ibotta works, and it’s surprisingly easy. In a nutshell, the app has a ton of rebate offers on grocery items and other essentials. You have to add the offers to your profile before heading to the store. But after you’ve finished shopping and have at least $20 in rebates, you can claim your money with a transfer through either PayPal or Venmo.

10. Consider a side hustle.

If making ends meet is hard enough as it is, with an emergency fund or savings feeling out of reach, it may be time to consider an extra gig to help meet your financial goals. There are even side hustle websites that can help you find remote work so you don’t have to leave home to land some extra cash.

Related: 101 Best Side Hustles for Earning Extra Cash

{kind=link}

Tell us what you think

We're having a little work done... Comments will be back soon!