Get all the new deals and savings hacks straight to your inbox

Will be used in accordance with our Privacy Policy

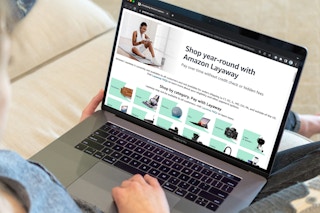

If your Amazon shopping is getting a little wild and your wallet is feeling the strain, check out the Amazon Layaway option. The beauty of their layaway program is that you can use it year-round, including Amazon’s big sale events like Prime Big Deal Days, Amazon Black Friday deals. Spoiler alert: With Amazon’s layaway, there’s absolutely no credit check, fees, or interest. And it locks in the price. With Amazon’s ever-changing pricing model, locking in the price when you see it drop is a great feature.

While there are plenty of buy-now-pay-later options on the market right now, it makes sense that Amazon has finally joined the club. We dug into the nitty-gritty details of the Amazon Layaway program to make it easy for you.

To get the best Amazon deals sent right to your phone, text AMAZON or SAVE to 57299 on your mobile device. Or, download the Krazy Coupon Lady app.

What is Amazon Layaway, and how does it work?

With Amazon Layaway, you can put 20% down on any eligible purchase and spread out the remaining four equal payments every two weeks over eight weeks. When the payment due date hits, they’ll automatically withdraw it from your credit or debit card. Any taxes or shipping fees are added to the last bill.

To take advantage of Amazon Layaway, make sure you’re logged into your Amazon account. When you find a deal you like, look for the “Reserve with Layaway” label or Payment plans (under Purchase options and add-ons) on the product page (or during checkout once you’ve added the item(s) to your cart) to find more details on layaway eligibility.

If you need to make any changes to your layaway payment plan, you can do it through your account page on Amazon.com. And if you’re feeling a little impatient about receiving your item or want your item shipped earlier, you can pay off the balance right then and there and it’ll arrive quicker.

Don’t worry about being stuck in a contract if you change your mind about the layaway payment plan, either. If you cancel, you’ll get a full refund on all payments.

TIP: Amazon also uses Zip (formerly Quadpay), where you can spread out your purchase in a series of four payments over six weeks. Unlike with Amazon Layaway, your order ships right away with Zip, as if you had paid in full. If you don’t mind a shorter term payment plan, this may be a better option for cheaper purchases. We did a deep dive into all of the buy-now-pay-later options available.

Does Amazon Layaway require a credit check?

No. Don’t worry about having to pass any kind of credit check. Unlike Amazon’s other buy-now-pay-later option Affirm, no credit check or credit is reported with the layaway program. You’ll also not incur any interest fees on late payments.

RELATED: Amazon Prime Day Invite-Only Program, Explained

Is Amazon Layaway available in all states?

Currently, the layaway program is not available in all U.S. states. If your shipping address is in Connecticut, Washington D.C., Illinois, Maryland, Ohio, or Pennsylvania, then you may have to wait a bit longer for it to roll out to your area.

TIP: For the next holiday season, if you want to get your gift by Dec. 25 with the layaway plan, remember to make your purchases by Oct. 23. Otherwise, you can opt to pay it off early to receive your item by then.

Amazon accepts all payments for layaway — except gift cards.

All major debit cards and credit cards are accepted when you opt for a layaway plan. However, Amazon will not accept gift cards as payment when you start the layaway plan.

What happens if I miss a layaway payment?

If you miss a payment, there will be no hit to your credit. Amazon will send you a reminder email with the overdue amount. If they don’t receive the payment by the time the next one is due, they’ll cancel the order and refund your previous charges.

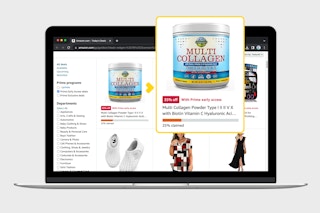

Layaway only works for eligible Amazon items (which is great during Amazon sales).

Layaway is only available for select items sold and shipped directly from Amazon. You can find the exact items available and a list of the categories on the Amazon Layaway shopping page. Eligible items include furniture, PCs, exercise equipment, and more.

You can use their layaway program during Prime Day and October Prime Day, too! So keep that in mind as you formulate your Prime Day shopping strategies.

Top layaway items in recent years include:

Sale items retain their price when you buy them through layaway.

Find something on sale or a Lightning Deal that you can’t pass up? Don’t fret about your layaway payment changing if the item’s price goes up. Whatever the product’s price is when you start the program, the cost will stay.

The layaway program is available all year — even on the coveted Amazon Prime Day and holidays. You can also return any items you’ve purchased with Layaway by following the standard Amazon return and exchange policies.

TIP: To find limited-time deals and Lightning Deals eligible for the layaway program, go to the category you’re most interested in under the layaway program page and filter by “Today’s Deals.”

Have more questions? Check out the FAQ on Amazon.com.

Download the KCL app to add and redeem coupons in store

For iOS and Android users.

Get all the new deals and savings hacks straight to your inbox

Will be used in accordance with our Privacy Policy