Get all the new deals and savings hacks straight to your inbox

Will be used in accordance with our Privacy Policy

Looking for a good way to combat inflation ? Even the best cash-back credit cards don’t usually make up for the entire 7.1% that inflation has taken out of your pocket over the past year, but they can make a serious dent. Most offer options that pay as much as 5% cash back , and one actually pays 8% – 10% on select purchases.

When you use a credit card, you really need to be careful how you use it. First, If you don’t pay off your balance in full every month, you could incur interest charges that eat away at the cash-back rewards and then some. Further, it could also raise your credit utilization, which can result in a lower credit score.

But if you’re following best practices, these rewards programs can be a net benefit. Below we’ll review the best cash-back credit cards out there. Bear in mind that to qualify for the most useful cards, you’re going to need great credit.

You won’t be able to get any of these specific cards unless you have good credit. This is considered to start somewhere between 670 and 700, depending on the lending institution. There’s even one card that won’t accept you unless you have “excellent” credit.

TIP: If you’re working your way up, check out the best cards for bad credit, then come back once you’ve bumped your score up. But if your credit report is ready for it, check out these cash-back cards to find out which is best for you.

And as usual, we recommend already downloading The Krazy Coupon Lady app for money-saving hacks.

1. Capital One SavorOne Cash Rewards

Capital One SavorOne Cash Rewards pays out the most. A card that pays more than 5% cash back is almost unheard of, but this unicorn exists. In select categories, you can earn 8% – 10% back with this card.

Capital One is picky with who gets this card. In addition to an excellent credit score, you’ll need:

-

No bankruptcies or loan defaults.

-

No history of being 60 days late on a credit card or medical bill.

-

A history of holding a loan or credit card for at least three years with a credit limit of $5,000+.

Pros

-

A cash-back rewards program that pays 8% – 10% in some categories is unparalleled.

-

Low minimum spend to earn the cash bonus offer.

-

Introductory rate on purchases and balance transfers brings costs down to zero for 15 months.

Cons

-

Highest cash-back offers are only available for very specific select categories.

-

You will need excellent credit to qualify. Excellent credit typically starts somewhere around 720 or 740.

Who is this card best for?

This card is for credit score champions. You’ll have to have a great credit score and near spotless credit history to qualify. If you do, you’ll get high cash rewards offers, but the best ones are only available for Uber spending (10%) and tickets you purchase through Capital One Entertainment (8%).

2. American Express Blue Cash Preferred

The American Express Blue Cash Preferred pays out a relatively large sign-up bonus and larger percentages for cash rewards. However, it does come with an annual fee. Moreover, keep in mind that while many merchants accept American Express, not all do.

Pros

-

One of the largest bonus offers currently available, though there’s a large minimum spend to match.

-

High cash-back rewards on groceries and select streaming services.

-

We hope you won’t make a late payment to incur the penalty APR, but if you do, it only lasts six months rather than in perpetuity.

Cons

-

$95 annual fee, though it is waived for the first year.

-

Shorter period for introductory APR than some of the others on this list — just 12 months compared to 15.

-

This card comes with a foreign transaction fee.

Who is this card best for?

This card is best for those who are willing to shut down their card before their first anniversary (which could ding your credit score) or are willing to pay a $95 annual fee after the first year.

You may find the fee pays for itself, though. For example, you can get 6% cash back on your first $6,000 spent on groceries every year. That’s a $500 spend every month, which might be a lot for a single person but is well under the average for a family of four. That comes out to $360/year in cash-back benefits just for groceries — far more than the $95 annual fee.

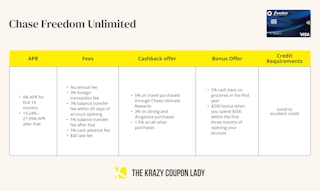

3. Chase Freedom Unlimited

Chase Freedom Unlimited is currently offering 5% cash back on up to $12,000 in groceries for the first year — or $600 cash back on groceries total. Plus, they also offer a reasonable $200 bonus if you meet the minimum spend of $500 within the first three months.

Pros

-

The base rewards are decent, but the fact that you get 5% cash back on groceries for the first year puts them over the top.

-

Low minimum spend to earn the sign-up cash bonus.

-

No annual fee.

Cons

-

There is a foreign transaction fee with this card.

-

Reduction on balance transfer fees doesn’t last nearly as long as the introductory APR.

Who is this card best for?

Simply put, this card is currently best for those with a high monthly spend on groceries. Getting maximum rewards on a $12,000 spend means buying at least $1,000 in groceries every month. Thanks to inflation, that’s not an unreasonable number for most families anymore.

After the first year, it’s best for those who regularly book travel through Chase Ultimate Rewards or those who dine out or shop at drugstores fairly regularly.

TIP: Are you a big traveler? You might want to check out Chase Sapphire Preferred.

4. Discover it Cash Back

Discover it Cash Back pays 1% on all purchases. But in select categories each quarter, you’ll get 5% cash back. For example, the categories for Q1 2023 were:

-

Groceries

-

Drug stores

-

Select streaming services

These rotating categories might affect your spending habits. Maybe you used PayPal for curbside grocery checkout in the past, but now you would use your Discover card directly to pay your grocer in app. That way you get the 5% cash back this quarter.

Pros

-

Discover will match your total cash back on your 1-year anniversary.

-

There’s no annual fee.

-

Discover is a bit more gracious than other lenders. They’ll give you one late payment without charging late fees.

Cons

-

Categories rotate each quarter, so you’ll have to keep track of them as you strategize your spend.

-

You’ll have to activate the quarterly bonuses for your 5%. If you forget, you won’t get it retroactively.

Who is this card best for?

Discover it is best for those who are okay with cash-back categories rotating quarterly. If you remember to activate it each quarter, it can mean big rewards. The card is also good for those who want a little grace, as they’ve branded themselves on that principle and work it into some of their policies.

5. Citi Custom Cash Card

The Citi Custom Cash Card is pretty amazing in that it ensures you get the highest possible cash back every month. You’ll get 5% rewards on whichever category you spend the most in any given billing cycle. The eligible categories are:

-

Restaurants

-

Gas stations

-

Groceries

-

Travel (select)

-

Transit expenses (select)

-

Streaming services (select)

-

Drugstores

-

Home improvement stores

-

Fitness clubs

-

Live entertainment

Pros

-

Rest assured that you’ll get 5% rewards in the most advantageous category each month.

-

No annual fee.

-

You have six months to meet the minimum spend for the sign-up bonus, while many other programs only give you three months.

Cons

-

This card does have a foreign transaction fee.

-

Cash bonus isn’t very high when you take the minimum spend into consideration.

-

Penalty APR can apply indefinitely if you miss a payment.

Who is this card best for?

The Citi Custom Cash Card is for those who want to get the most rewards without having to think about it too much. Citi customizes their rewards to you instead of you having to strategize your shop.

It might not be great for you if you spend a significant amount of time overseas or you want a larger sign-up bonus.

6. Chase Freedom Flex

In addition to three fixed cash-back tiers, Chase Freedom Flex gives you 5% cash back on extra rotating categories each quarter. For example, the categories for Q1 2023 are:

-

Grocery stores (excludes Walmart)

-

Target

-

Fitness clubs

-

Gym memberships

Pros

-

Lots of opportunities to earn cash back.

-

Low minimum spend required for signup bonus offer.

-

No annual fee.

Cons

-

Balance transfer fee is reduced for first 15 months, but not eliminated.

-

If you incur the penalty APR by being late on a payment, it could stick around forever.

Who is this card best for?

You’ll get the most out of this card if you frequently book travel through Chase Ultimate Rewards, dine out a lot, or frequent drugstores. However, the rotating categories can help make sure almost anyone is covered throughout the year.

7. US Bank Cash+ Visa Signature Card

The US Bank Cash+ Visa Signature card allows you to pick which categories you want to use for your 5% cash back. In addition to travel made through US Bank’s Rewards Travel Center, you get to pick two more categories from the below to earn 5% cash back:

-

Fast food

-

Home utilities

-

TV, internet, and streaming services

-

Cell phone bills

-

Department stores

-

Electronic stores

-

Sporting good stores

-

Gym memberships and fitness clubs

-

Ground transportation

-

Movie theaters

-

Furniture stores

-

Select clothing stores

Then you’ll get to pick another category to earn 2% cash back from the below:

-

Groceries

-

Restaurants

-

Gas stations and EV charging stations

Pros

-

You get to pick two 5% cash-back categories each quarter.

-

You also get to pick which category you want for the 2% cash back each quarter.

-

No annual fee.

Cons

-

Minimum spend is a bit high considering the amount of the sign-up bonus. It’s not unachievable, but if you don’t think you’ll spend $1,000 on your card in four months, there are other options.

-

No reduction in the balance transfer fee as a part of the introductory offer.

Who is this card best for?

This card is best for those who want to pick their rewards. It’s like a choose-your-own-adventure story for cash-back credit cards. This card isn’t well suited for those who spend significant time abroad, as it does come with foreign transaction fees.

Related: 7 Best Travel Rewards Credit Cards

8. Capital One Quicksilver Cash Rewards

Capital One Quicksilver Cash Rewards doesn’t come with a cash sign-up bonus, but it does give you a generous 3% on each and every purchase you make during the first year. After that, the “all purchases” category reverts to 1.5%, which is slightly better than the 1% offered by most other cards.

Pros

-

3% cash back on all purchases made within the first year is a generous offer.

-

After the first year, cash back on all purchases reverts to 1.5%, which is still higher than the 1% most cards offer on catch-all categories.

-

No balance transfer fee for first 15 months.

-

There is no annual fee.

Cons

-

While there is a cash-back multiplier for the first year, there’s no sign-up cash bonus.

-

The highest cash-back category — travel — only earns points for hotels and rental cars you book through Capital One.

Who is this card best for?

For the first year, this card is best for those that want decently high rewards on all their everyday purchases. Three percent is a high floor, and you benefit. After that first year, it’s best for those who regularly book hotels and rental cars through Capital One.

Cash-Back Card FAQs

How does a cash-back credit card work?

When you make purchases on your credit card in certain spending categories, cash-back cards put a percentage back in your pocket. Some issue cash-back rewards as a statement credit, while others allow you to cash out to your bank account or issue your rewards as an Amazon credit.

How do I pick the best cash-back credit card for me?

To pick the best cash-back card for your situation, you’ll need to be acutely aware of your spending habits each month. Most budgeting apps can track your spending if you let them run for a month or two.

Once you know where you spend the most money, you can find a card that offers the most cash back for your highest spending categories. Other factors to take into consideration include:

-

Is there an annual fee?

-

What about a cash sign-up bonus offer?

-

Is my credit good enough to qualify for this card?

-

Do I travel out of the country a lot? If so, is there a foreign transaction fee?

Is a 1.5% cash-back credit card good?

A few years ago, 1.5% cash back would have been a great offer. Even today, if you’re getting 1.5% cash back on “all other purchases,” that’s still an above-average offer.

But today, the best cash-back credit cards generally offer 3% – 5% cash back in select categories. The Capital One SavorOne Cash Rewards card even offers 8% – 10% cash back for some purchases!

How do I get the most cash back on my credit card?

The best way to get the most cash back on your credit card is to strategize your spend according to the highest paying categories. If you have more than one card, you can even use different cards to pay for different expenses accordingly.

Another important thing to do is pay your balance in full and on time each and every time. If you incur any interest, you’ll be wiping out the benefits you get from any cash-back program.

What are the different categories of cash-back credit cards?

There are four different categories of cash-back credit cards:

-

Flat rate: These cards pay you one flat rate on all purchases, with no special spending categories. In today’s market, 1.5% cash back is the minimum you should look for with flat rate cards, and you can aim for cards with 2% cash back or more.

-

Tiered rate: These cards will give you a different rate for different categories, but those rates are fixed year-round. For example, you might get 5% on travel purchases, 2% on groceries, and 1% on everything else.

-

Rotating categories: These cards tend to offer you a higher cash-back amount on rotating spending categories throughout the year, then a lower percent (like 1%) back on all other purchases. A good example is Discover it Cash Back.

Store cards: These cards can usually only be used at the store that branded them, but sometimes if you have a high enough credit score, you can get a cash-back store card useable anywhere. A good example is the entire suite of Amazon credit cards, and the many variations of the Target RedCard .

Download the KCL app to add and redeem coupons in store

For iOS and Android users.

Get all the new deals and savings hacks straight to your inbox

Will be used in accordance with our Privacy Policy