Gift cards are truly the gifts that keep on giving. However, gift card hacks can save money on the things you want, too. #everyoneshappy.

There are a few easy places to pick up discounted gift cards (that means cards that are priced less than their value). We found that buying and using discounted gift cards can save an average of 12% – 15%. Deeply discounted gift cards are harder to come by, but we have seen some savings up to 54% (call those unicorns).

A few of our favorite sites to scour for discount gift cards include Gift Card Granny and Raise. These online sources have a range of retailer gift cards up for grabs, each priced below what the card is worth. Essentially, they buy unwanted gift cards and then turn around and sell them for less to people like us.

We’ve rounded up the ways in which you can get more out of a gift card than you could have ever imagined.

Download The Krazy Coupon Lady app so you never miss out on the best tips and discounts.

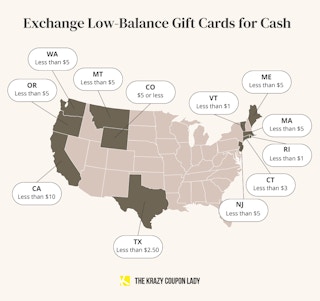

1. Exchange low-balance gift cards for cash.

Did you know that if you live in certain states, by law you can exchange gift cards for cash? It’s pretty much at the top of our ultimate list of gift card hacks.

It’ll work for any retail or restaurant gift card, but not on bank-issued cash cards like Visa.

This trick also excludes promotional gift cards (like #3).

2. Stock up on gift cards in January.

Think of it like Christmas overflow.

Thousands of people receive gift cards for Christmas that they don’t want, so they sell them on discounted gift card sites.

Because supply will outweigh demand following Christmas, you’ll see some outstanding deals.

3. Buy restaurant gift cards in December.

Gift card hacks happen every holiday season. During December, restaurants offer tons of “free gift cards with a purchase” deals.

Usually the free promotional gift card isn’t redeemable the same day, and in some cases, you need to wait a week or longer to redeem.

4. Combine discounted gift cards with coupon deals to save even more.

Pay with a discounted gift card, and you just upped your savings even more.

Since diaper deals happen at least once every three months or more, I buy Rite Aid, CVS, or Walgreens discounted gift cards and combine them with coupons when I see a good sale on diapers.

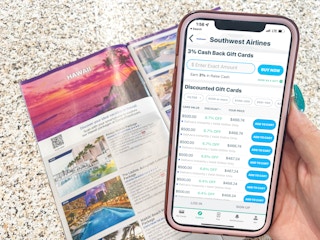

5. Use discounted gift cards for travel.

Gift cards hacks aren’t just useful for mall shopping anymore.

Save money on travel and entertainment by buying discount gift cards for airlines, hotels, and restaurants online at Raise.com, GiftCardGranny.com, or in store or online at SamsClub.com and Costco.com .

Current Southwest Airlines gift card deal at Costco:

Related: Black Friday Freebies

6. Purchase movie tickets with gift cards.

Gift cards for movie theaters and ticket sales outlets are HUGE on discount gift card sites. For example, on Raise we found Fandango gift cards for 14.4% off. Stack this with Tuesday movie deals and you’re saving even more on your movie tickets!

7. Use the Raise app to buy the eGift card you want to use while you’re waiting in line to pay.

We love the Raise app.

You can purchase a gift card while standing in line and it’ll be available to use by the time you’re ready to pay.

The Raise app will also track gift card balances and keep all your cards readily available in your app wallet.

8. Don’t purchase discounted gift cards more than three months in advance.

Raise offers a 1-year guarantee on your newly purchased card balance and usability but 90 days for physical gift cards not received.

After that, if there are any problems with the card, you’re on your own!

9. Sort cards by the “highest discount” when buying gift cards from Raise.

Use the “sort” feature to see the highest discounted cards first. Then work your way through the list until you spot what you want.

10. Use Williams-Sonoma gift cards at West Elm to get the best discounts.

Gift card hacks 101 — higher-end stores like West Elm won’t have heavily discounted gift cards (usually under 4%), but you can sometimes get better discounts on gift cards for their sister stores!

The best part is that many sister stores accept each others’ gift cards, so learn to work that system.

Here are a few stores that accept each others’ gift cards:

-

Gap , Gap Kids, Old Navy , Banana Republic , and Athleta

-

Walmart and Sam’s Club (including Walmart Gas and Sam’s Club Gas)

-

PBteen, Pottery Barn Kids, Pottery Barn, West Elm, Mark and Graham, and Williams-Sonoma

-

J.Crew, J.Crew Factory, J.Crew Mercantile, crewcuts

-

Outback Steakhouse, Carrabba’s Italian Grill, Bonefish Grill

-

Kroger brand stores (Kroger, Barclay Jewelers, Baker’s, City Market, Copps, Dillons, Food 4 Less, Foods Co., Fred Meyer, Fred Meyer Jewelers, Fresh Eats, Fry’s Food and Drug, Gerbes, Jay C, King Soopers, Littman Jewelers, Mariano’s, Metro Market, Owen’s, Pay Less Supermarkets, Pick ‘n Save, QFC, Ralphs, Smith’s Food and Drug, and Turkey Hill Experience)

-

Darden Restaurants: Olive Garden, Bahama Breeze, Red Lobster, LongHorn Steakhouse, Season 52, The Capital Grille, and Yard House

When shopping the Gift Card Granny website (on your computer), look to the bottom left side of your screen — it’ll tell you if the cards are accepted at other stores.

11. Set an email alert at Raise.com and get notified when an out-of-stock gift card you want is available.

Want your favorite brand at a certain discount? Sign up for email brand alerts at Raise.com so you never miss a deal.

When the alert does come through, buy immediately! We can’t stress this enough — once back in stock, gift cards often sell immediately because others are waiting for them too!

12. Earn free gift cards with the Gift Card Granny Rewards Program.

With the Granny Rewards program, you can earn cash back when you register for a Gift Card Granny account, sign up for their newsletter, buy gift cards marked cash back, and when you make your first purchase. Once you have $10 in your account, you can cash out or redeem your cash back in a gift card.

13. Get 15% off your first gift card purchase on Raise.com.

You’ll get a $10 discount code emailed to you when you sign up for the Raise newsletter. Plus, you get 15% off your first purchase, no spend threshold required. You can’t combine these two discounts on one purchase.

14. Don’t buy physical gift cards from discounted gift card websites.

Physical gift cards can take a few weeks to receive in the mail, and some sites even charge for shipping. If you do need a physical gift card, buy it from Raise, since they offer free shipping. Remember, Raise’s money back guarantee doesn’t cover physical cards you don’t receive.

Instead, get an electronic eGift card or voucher to use instantly.

15. Get about $0.80 on the dollar when you sell your unwanted gift card.

Received cards you don’t want?

Raise and Gift Card Granny won’t pay your card’s full value, but you’ll get cash with no strings attached.

Most cards will get you an average of $0.80 on the dollar, but the most popular brands ( Walmart , Amazon , and Target ) can be sold for as much as 96 – 99% of their cash value. Raise takes 15% from your selling price when your card sells.

If you have a gift card you know you won’t use, this is a great option.

16. Buy discounted physical gift cards at Costco and Sam’s Club.

Sam’s Club and Costco carry discounted gift cards for movie tickets and restaurants like Ruth’s Chris, Build-A-Bear, entertainment gift cards for movie tickets and streaming, and travel gift cards from Southwest Airlines .

Current in-store deal at Costco:

17. If you have a physical card, take a photo of the back.

As far as gift card hacks go, this one is pretty clever. If you lose the card, you can still redeem it as long as you know the numbers from the back of the card, provided someone hasn’t used it.

18. Redeem credit card points for gift cards.

Most credit card reward programs allow you to redeem points for gift cards.

19. Stack discounted gift cards to complete your purchase.

If you have multiple gift cards for the same retailer (or sister store — see #10), stack them to pay 100% of your purchase.

Some retailers do have limits. For example, eBay will only take four cards, and Gap will take up to five cards.

20. Buy regular items at Target and get free $5 – $20 Target gift cards.

Target deals totally rock. Frequently, you can get a free $5 – $20 Target gift card for purchasing certain items.

For example, we’ve seen deals where you can get a free $20 gift card with purchase of select baby formula 6-packs.

21. Get up to 50% off gift cards on LivingSocial and Groupon.

For example, 25,000 people paid $10 for a $20 Target card when Groupon ran the deal.

22. Get paid in gift cards when you use Ibotta.

If you aren’t already using Ibotta ( one of our top favorite apps ), you should be. You can get cash back for just buying groceries at retailers including Meijer , Kroger , Walmart , Aldi , Walgreens , Dollar General , and more.

You’ll get an immediate $5 after redeeming your first rebate and another $10 every time you refer a friend. You can withdraw your earnings once you reach $20 in gift cards for places like Amazon , Best Buy , Target , Starbucks, and more, or make a deposit to your PayPal or bank account.

23. Carry a Sharpie to track your physical card balance.

If you use physical cards, here’s one of the easiest gift card hacks. Track balances by writing the leftover amount on the card with a permanent marker so you don’t have to keep checking your balance online.

24. Add credit to your Amazon account with small-balance Visa cards.

Already know that you’ll forget about that low-balance Visa cash card in your wallet?

Turn it into Amazon credit by doing the following:

-

Let’s say your Visa card has a balance of $3.01. Use it to buy a $3.01 Amazon eGift card (you can purchase them for any amount, starting as low as $1).

-

Apply the Amazon eGift card to your Amazon account.

-

BAM! It’ll show up as credit for your next purchase.

25. Track eGift card and voucher balances on the Raise app.

Use the Raise app to track your eGift card and voucher balances.

Download the KCL app to add and redeem coupons in store

For iOS and Android users.